JSC National Atomic Company “Kazatomprom” (“Kazatomprom”, “KAP” or “the Company”) announces the following operations and trading update for the third quarter and nine months ended 30 September 2021.

This update provides a summary of recent developments in the uranium industry, as well as provisional information related to the Company’s key third-quarter and nine-month operating and trading results, and current 2021 guidance. The information contained in this Operations and Trading Update may be subject to change.

Market Overview

The International Atomic Energy Agency’s (IAEA) latest projections for 2050 were released, highlighting nuclear power as a reliable and clean source of energy that can effectively help the world reduce reliance on fossil fuel sources in the fight against climate change. According to IAEA Director General Rafael Mariano Grossi, “The updated IAEA projections show that nuclear power will continue to play an indispensable role in low carbon energy production”. The Agency’s previous high-case projection that assumed 715 GWe of generation capacity from nuclear in 2050, was revised up by just over 10%, to 792 GWe by 2050, compared to 393 GWe in 2020. The IAEA’s high-case, now showing a near doubling of nuclear capacity by 2050, is close to the International Energy Agency’s projections in their publication “Net Zero by 2050 – A Roadmap for the Global Energy Sector”. The low-case from the IAEA’s updated report assumes that world nuclear capacity in 2050 could remain essentially unchanged from current levels.

In geopolitical policy developments, Japan’s governing Liberal Democratic Party with its new leader, Prime Minister Fumio Kishida, reconfirmed its support for additional restarts in the country’s nuclear sector. Drafted under former Prime Minister Yoshihide Suga, Japan's new basic energy plan targets a 20%-22% share of nuclear generation in 2030.

In another positive, high-level policy development, UK Prime Minister Boris Johnson confirmed his government’s commitment to decarbonize UK power system by 2035. The UK government is expected to focus its efforts on the deployment of a new generation of domestic technologies, including nuclear, wind, solar, hydrogen, and carbon capture, utilization and storage (CCUS).

Meanwhile, French President Emmanuel Macron announced a €30 billion investment plan designed to reduce carbon emissions and revitalize the country’s industrial sector, aiming to make France a global innovation leader in areas including green industry, healthcare, and digital and bio technology, by 2030. Of note, €1 billion has been allocated for the development of small modular and innovative nuclear reactors with improved waste management.

Finally, in the US, Illinois’ comprehensive energy legislation, the Climate and Equitable Jobs Act, was signed by Governor JB Pritzker, requiring the state to reduce its emissions by 45% no later than 2038 and achieve a 100% zero-emissions power sector by 2045. The Act includes nearly US$700 million in new state subsidies over the next five years, allowing for the continued operation of Exelon’s Byron and Dresden nuclear power plants that were under threat of closure, with further support for its Braidwood nuclear plant.

A number of demand-side highlights emerged in the third quarter:

- In September 2021, Nawah Energy Company, the Emirates Nuclear Energy Corporation’s operating and maintenance subsidiary, announced the successful connection of the Barakah unit 2 APR-1400 reactor to the UAE grid.

- China National Nuclear Corporation announced the extension of the operating license for the country’s oldest nuclear power reactor, Qinshan unit 1, in Zhejiang province, eastern China. Under the extended license, the 350MWe CNP-300 PWR will operate until July 2041.

- Asco units 1 and 2 in Tarragona, Spain, owned by Endesa and Iberdola, have been granted ten-year operating license extensions. Unit 1 is authorized to operate until October 2030, while unit 2’s license is renewed until October 2031. The Asco plant is one of Spain’s five operational nuclear facilites and comprises two 1030MWe PWR units.

- According to Taiwan Power Company, Kuosheng unit 1, a 985 MWe BWR, was permanently shut down and entered decommissioning in July 2021, following 40 years of safe power production. The plant's second unit is scheduled to operate until March 2023, at which point its 40-year operating permit expires.

- Pakistan Atomic Energy Commission announced that in August, Karachi unit 1, a 125 MWe CANDU reactor, was shut down after 49 years of operation. The closure follows the commissioning of Karachi unit 2, a 1,100 MWe Chinese-designed HPR1000 reactor, earlier this year.

Outside of the demand-related announcements from various end-users that consume uranium products, increased near-term activity from financial investment vehicles that focus on holding physical uranium – “unconventional demand” – also generated notable highlights. The most significant development was the completion of Sprott Asset Management LP’s acquisition of Uranium Participation Corporation (UPC) in July, and the subsequent Toronto-listing of the Sprott Physical Uranium Trust (SPUT). SPUT took ownership of UPC’s existing inventory of 18.1 million pounds U3O8 and through an at-the-market offering, SPUT embarked on an aggressive, ongoing purchasing campaign using the proceeds from interested investors who can buy SPUT trust units on an ongoing basis. The offering, through which SPUT could currently deploy as much as US$1.3 billion from its investors to lock away near- and medium-term primary production and secondary supplies, had funded the purchase of more than 11 million pounds U3O8 by the end of the quarter. Including the uranium from its acquisition of UPC, SPUT’s total holdings were more than 29 million pounds U3O8 at 30 September 2021.

Also in the category of unconventional demand, UK-based Yellow Cake Plc made purchases in the near-term market, increasing their uranium holdings by more than 2.5 million pounds U3O8 in the third quarter, for a total position of nearly 14 million pounds U3O8.

Subsequent to the end of the third quarter:

- SPUT, funded by its ATM offering, continued to purchase physical uranium in the near-term market throughout October, adding 6 million additional pounds of uranium to its holdings.

- Yellow Cake Plc announced a share placement to raise gross proceeds of approximately US$150 million, with which it intends to purchase approximately 3 million additional pounds of uranium (1 million pounds from Kazatomprom and 2 million pounds from Curzon Uranium Limited).

- Kazatomprom announced its investment in ANU Energy OEIC Ltd (the Fund), established on the Astana International Financial Centre (AIFC). The Fund will hold physical uranium as a long-term investment with its initial purchases financed through a founder’s round investment totaling US$50 million, sourced from Kazatomprom at 48.5%, National Investment Corporation of the National Bank of Kazakhstan at 48.5%, and Genchi Global Limited (the Fund Manager) at 3%. Once operating, the Fund could raise up to US$500 million to purchase additional uranium. ANU Energy will be the first fund providing emerging market investors, particularly those focused on ESG and clean energy, with direct access to a locally-based physical uranium investment.

As is commonly the case over the quieter summer months, there were no notable third-quarter developments on the supply side.

Market Pricing and Activity

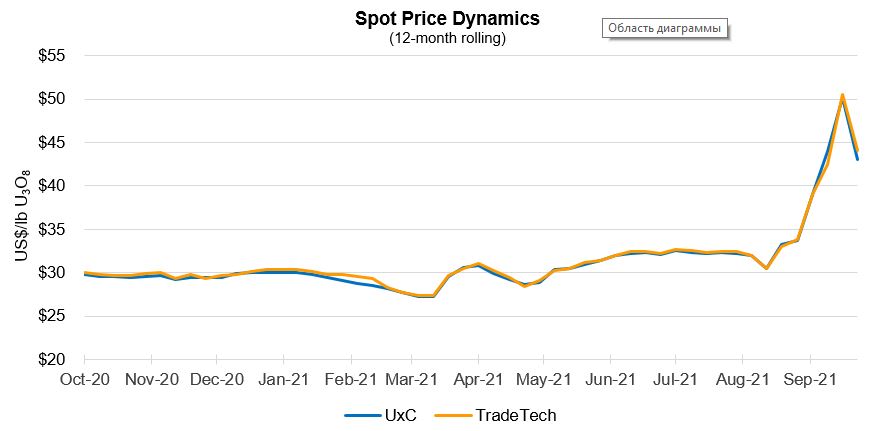

The spot market is typically quiet over the summer months and activity was expectedly low through the first half of the third quarter, with spot price remaining in the low US$30/lb U3O8 range. However, once the Sprott Physical Uranium Trust was established and operating, entering the market to buy uranium almost daily through the second half of August and into September, the spot price reacted, increasing rapidly as near-term supplies tightened quicker than many market participants expected. The spot price rose to just over US$50.00/lb U3O8 in late September, and when activity slowed significantly following uncertainty across the broader equity markets, the price decreased to about US$43.00/lb U3O8 by the end of the quarter.

According to third-party market data, spot volumes transacted over the first nine months of 2021 were 9% higher compared to the same period last year. A total of approximately 70.9 million pounds U3O8 (27,300 tU) was transacted at an average weekly spot price of US$31.96/lb U3O8 (compared to about 65.1 million pounds U3O8 (25,000 tU) at an average weekly spot price of US$29.56/lb U3O8 during the the first nine months of 2020).

In the term market, third-party data indicated that contracted volumes totalled about 52.5 million pounds U3O8 (20,200 tU) through the first nine months of 2021 (compared to about 39.0 million pounds U3O8 (15,000 tU) in the same period of 2020). The 35% increase in term contracting activity to date in 2021 compared to last year, led to a significant US$7.50/lb U3O8 increase of the long-term price indicator at the end of the third quarter, averaging a five-year high of US$42.50/lb U3O8 (reported on a monthly basis by third-party sources).

Company Developments

COVID-19 Update

While delta-variant COVID-19 cases rose in parts of Kazakhstan in July, the second half of August saw the situation stabilize and government-mandated restrictions were partially relaxed. Kazatomprom continues to carefully monitor the COVID-19 situation to ensure current protections and protocols remain effective. Health-related pandemic risks have remained well mitigated within the Company in 2021 and if a case of COVID-19 is detected, proactive and preventive measures are implemented to contain the spread, with the health of the individual being constantly monitored and assistance provided as necessary.

Vaccination status is being monitored on a daily basis, with the Company’s vaccination level far exceeding that of the country (Kazakhstan had approximately 40% of its population fully vaccinated as at 28 October 2021). To date, each of the Group’s uranium mining entities has surpassed the 90% level of partially immunization coverage, with several sites now 100% fully vaccinated. Taken as a whole, including the corporate headquarters and all Group entities, as of 28 October 2021, 92% (17,962) of employees are partially vaccinated, with more than 89% fully vaccinated.

Kazatomprom’s Executive Board

As previously disclosed in September, the Company’s Board of Directors approved the appointment of Mr. Mazhit Sharipov as Kazatomprom’s Chief Executive Officer, following the resignation of Mr. Galymzhan Pirmatov on 27 August 2021. Additional changes to the senior management team were also approved by the Company’s Board of Directors (all previously announced), with the Company’s Management Board composition and management biographies now available at www.kazatomprom.kz.

Sale of MK KazSilicon LLP

On 20 October 2021, Kazatomprom conducted an auction to sell 100% of the authorized share capital of MK KazSilicon LLP through an electronic auction on the web portal of the state property. The auction was carried out in accordance with the Law of the Republic of Kazakhstan on the Sovereign Wealth Fund and the Rules for conducting electronic trading on the web portal of the state property register. The estimated value of MK KazSilicon LLP was 240 million tenge as determined by an independent, Big Four consultant. In accordance with the protocols of the auction, the winning bid amounted to 651,903,917 tenge. The sale of the asset was carried out as a part of of the Comprehensive Privatization Plan for 2021–2025, approved by the Government of the Republic of Kazakhstan.

Kazatomprom’s 2021 Third-Quarter Operational Results1

|

|

Three months ended September 30 |

|

Nine months ended September 30 |

|

||

|

(tU as U3O8 unless noted) |

2021 |

2020 |

Change |

2021 |

2020 |

Change |

|

Production volume (100% basis)2 |

5,508 |

4,657 |

18% |

15,960 |

15,091 |

6% |

|

Production volume (attributable basis)3 |

2,928 |

2,518 |

16% |

8,792 |

8,309 |

6% |

|

Group sales volume4 |

2,215 |

5,638 |

-61% |

8,409 |

9,857 |

-15% |

|

KAP sales volume (incl. in Group)5 |

1,619 |

4,975 |

-67% |

6,798 |

8,724 |

-22% |

|

KAP average realized price (USD/lb U3O8)6* |

31.68 |

30.45 |

4% |

29.99 |

29.58 |

1% |

|

Average month-end spot price (USD/lb U3O8)7* |

35.98 |

31.08 |

16% |

31.96 |

30.00 |

7% |

1 All values are preliminary.

2 Production volume (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it therefore disregards the fact that some portion of that production may be attributable to the Group’s joint venture partners or other third party shareholders. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

3 Production volume (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, which corresponds only to the size of such interest; it therefore excludes the remaining portion attributable to the JV partners or other third party shareholders, except for production from JV “Inkai” LLP, where the annual share of production is determined as per the Implementation Agreement disclosed in the IPO Prospectus. Actual drummed production volumes remain subject to converter adjustments and adjustments for in-process material.

4 Group sales volume: includes Kazatomprom’s sales and those of its consolidated subsidiaries (companies that KAP controls by having (i) the power to direct their relevant activities that significantly affect their returns, (ii) exposure, or rights, to variable returns from its involvement with these entities, and (iii) the ability to use its power over these entities to affect the amount of the Group’s returns. The existence and effect of substantive rights, including substantive potential voting rights, are considered when assessing whether KAP has power to control another entity).

5 KAP sales volume (incl. in Group): includes only the total external sales of KAP HQ and Trade House KazakAtom AG (THK). Intercompany transactions between KAP HQ and THK are not included.

6 KAP average realized price: the weighted average price per pound for the total external sales of KAP HQ and THK. The pricing of intercompany transactions between KAP HQ and THK are not included.

7 Source: UxC LLC, TradeTech. Values provided are the average of the month-end uranium spot prices quoted by UxC and TradeTech, and not the average of each weekly quoted spot price throughout the month. Contract price terms generally refer to a month-end price.

* Note the conversion of kgU to pounds U3O8 is 2.5998.

Production on both a 100% and attributable basis was higher for the first nine months of 2021 compared to the same period in 2020, and notably higher for the third quarter compared to the same period in 2020. The pandemic-related safety measures that were implemented in 2020 impacted production volumes throughout the second half of that year – production in 2020 should therefore be considered exceptionally low.

Uranium sales at both the Group and KAP levels decreased for both the third quarter and first nine months due to the timing of customer requirements and differences in the timing of deliveries in 2020 and 2021. The Company is able to forecast annual delivery expectations, though customers direct the specific timing of delivery within the calendar year.

Higher uranium prices in 2021 had a positive impact on Kazatomprom’s average realized price compared to 2020. If prices remain higher than 2020 through to year-end, the trend of increasing average realized price is expected to continue, with the Company’s delivery schedule weighted to the second half of 2021.

Kazatomprom’s 2021 Guidance

|

(exchange rate 430 KZT/1USD) |

2021 |

|

Production volume U3O8 (tU) (100% basis)1 |

21,700 – 22,0002 (previously 22,500 – 22,800) |

|

Production volume U3O8 (tU) (attributable basis)3 |

11,800 – 12,0002 (previously 12,100 – 12,400) |

|

Group sales volume (tU) (consolidated)4 |

16,300 – 16,800 (previously 15,500 – 16,000) |

|

Incl. KAP sales volume (incl. in Group) (tU)5 |

13,500 – 14,000 |

|

Revenue - consolidated (KZT billions) |

660 – 6706 (previously 620 – 640) |

|

Revenue from Group U3O8 sales, (KZT billions) |

540 – 5606 |

|

C1 cash cost (attributable basis) (USD/lb)* |

$9.50 – $10.50 (previously $9.00 – $10.00) |

|

All-in sustaining cash cost (attributable C1 + capital cost) (USD/lb)* |

$13.50 – $14.50 (previously $13.00-$14.00) |

|

Total capital expenditures of mining entities (KZT billions) (100% basis)7 |

90 – 100 |

1 Production volume U3O8 (tU) (100% basis): Amounts represent the entirety of production of an entity in which the Company has an interest; it disregards that some portion of production may be attributable to the Group’s JV partners or other third-party shareholders.

2 The duration and full impact of the COVID-19 pandemic is not yet known. Annual production volumes could therefore vary from our expectations.

3 Production volume U3O8 (tU) (attributable basis): Amounts represent the portion of production of an entity in which the Company has an interest, corresponding only to the size of such interest; it excludes the portion attributable to the JV partners or other third-party shareholders, except for JV “Inkai” LLP, where the annual share of production is determined as per Implementation Agreement as disclosed in IPO Prospectus.

4 Group sales volume: includes Kazatomprom’s sales and those of its consolidated subsidiaries. Volume does not include approximately 225 tU equivalent expected to be delivered as UF6 in 4Q21.

5 KAP sales volume: includes only the total external sales of KAP HQ and THK. Intercompany transactions between KAP HQ and THK are not included. Volume does not include approximately 225 tU equivalent expected to be delivered as UF6 in 4Q21.

6 Revenue estimates have only been updated to account for a change in expectations for consolidated 2021 uranium sales. Revenue expectations are based on uranium prices taken at a single point in time from third-party sources. The prices used do not reflect any internal estimate from Kazatomprom, and 2021 revenue could be materially impacted by how actual uranium prices and exchange rates vary from the third-party estimates.

7 Total capital expenditures (100% basis): includes only capital expenditures of the mining entities.

* Note that the conversion of kgU to pounds U3O8 is 2.5998.

Kazatomprom’s 2021 production expectations have decreased due to delays in exploration and wellfield development activity. Pandemic-related supply chain issues have resulted in limited access to certain key operating materials and equipment (production reagents, certain types of pipes and pumps, specialized equipment, drilling rigs), which has had a material impact on the Company’s production schedule. On a 100% basis, the Company now expects to produce between 21,700 – 22,000 (previously 22,500 – 22,800) and on an attributable basis, 11,800 – 12,000 (previously 12,100 – 12,400).

The year-to-date supply chain delays have resulted in a shift of approximately 800 tU production (100% basis) into future periods, and the production shortfall is expected to be recovered over the life of mine at the impacted assets. Mine plans related to future periods have not yet been developed, so specific period(s) in which the production shortfall can be recovered is not yet known. Uncertainly in the production plans relate to the operational challenges created by the ongoing supply chain limitations that remain partially unresolved at this time.

Expected annual sales at the Group level has increased to between 16,300 – 16,800 (previously 15,500 – 16,000) due to additional sales by consolidated subsidiaries to JV partners. KAP sales volume remains within the previously expected range.

The Company’s expectation for attributable C1 cash cost (C1) has increased to between US$9.50/lb – US$10.50/lb (previously US$9.00/lb – US$10.00/lb) and all-in sustaining cash cost (AISC) has increased to between US$13.50/lb – US$14.50/lb (previously US$13.00/lb – US$14.00/lb). The expected increase is due to the lower planned production volume for 2021 and an overall increase in production costs related to the pandemic, with shipping and availability constraints resulting in higher costs to acquire operating materials. Year-end C1 and AISC may differ from the expected ranges if wellfield development, procurement and supply chain issues, including inflationary pressure on production materials, continues or becomes more pronounced in the fourth quarter.

Guidance for total capital expenditures of mining entities (100% basis) remains unchanged.

Revenue, C1 cash cost (attributable basis) and AISC may vary from the ranges shown, to the extent that the KZT-to-USD exchange rate and uranium spot prices differ from the Company’s original assumptions for 2021.

Note that the Company only updates annual guidance metrics in relation to operational factors and internal changes that are within its control. Key assumptions used for external metrics, including exchange rates and uranium prices, are established from third-party sources during the Company’s annual budget process. Such assumptions will only be updated on an interim basis in exceptional circumstances.

The Company continues to target an ongoing inventory level of approximately six to seven months of annual attributable production. However, inventory could fall below these levels in 2021 and 2022, due to COVID-related production losses. As such, during the third quarter, several transactions to purchase material in the spot market were carried out and the Company will continue to monitor market conditions for opportunities to optimise its inventory levels.

Conference Call Notification (12 November 2021)

Kazatomprom will be hosting a conference call to introduce the investment community to its new Chief Executive Officer, Mr. Mazhit Sharipov, and its new Chief Operating Officer, Mr. Aslan Bulekbay. The call will be hosted online via the Zoom platform, with Russian and English translation.

The call will begin at 17:00 (AST) / 11:00 (GMT) / 06:00 (EST). Following management remarks, an interactive Russian/English Q&A session will be held with investors.

Note that this call is intended to introduce the Company’s new CEO and COO and discuss strategic and operational matters. Kazatomprom formally reports its detailed financial information on an annual and half-year basis; quarterly financial information will therefore not be provided or reviewed on this call.

Interested parties are invited to join using the following link and details:

Join Zoom Meeting https://zoom.us/j/99710280736?pwd=M3ltMndDb21MUFdiUGxCenNwOVk1Zz09

Meeting ID: 997 1028 0736

Passcode: HtfWr3

International dial-in access for Zoom can be found here: https://zoom.us/u/ac4s3LFL4g

A recording of the video conference call will also be available at www.kazatomprom.kz after it concludes.

For further information, please contact:

Kazatomprom Investor Relations Inquiries

Cory Kos, Director of Investor Relations

Tel: +7 (8) 7172 45 81 80

Email: ir![]() kazatomprom.kz

kazatomprom.kz

Kazatomprom Public Relations and Media Inquiries

Torgyn Mukayeva, Chief Expert of GR & PR Department

Tel: +7 (8) 7172 45 80 63

Email: pr![]() kazatomprom.kz

kazatomprom.kz

About Kazatomprom

Kazatomprom is the world's largest producer of uranium, with the Company’s attributable production representing approximately 23% of global primary uranium production in 2020. The Group benefits from the largest reserve base in the industry and operates, through its subsidiaries, JVs and Associates, 26 deposits grouped into 14 mining assets. All of the Company’s mining operations are located in Kazakhstan and extract uranium using ISR technology with a focus on maintaining industry-leading health, safety and environment standards.

Kazatomprom securities are listed on the London Stock Exchange, Astana International Exchange, and Kazakhstan Stock Exchange. As the national atomic company in the Republic of Kazakhstan, the Group's primary customers are operators of nuclear generation capacity, and the principal export markets for the Group's products are China, South and Eastern Asia, Europe and North America. The Group sells uranium and uranium products under long-term contracts, short-term contracts, as well as in the spot market, directly from its headquarters in Nur-Sultan, Kazakhstan, and through its Switzerland-based trading subsidiary, Trade House KazakAtom AG (THK).

For more information, please see the Company website at http://www.kazatomprom.kz

Forward-looking statements

All statements other than statements of historical fact included in this communication or document are forward-looking statements. Forward-looking statements give the Company’s current expectations and projections relating to its financial condition, results of operations, plans, objectives, future performance and business. These statements may include, without limitation, any statements preceded by, followed by or including words such as “target,” “believe,” “expect,” “aim,” “intend,” “may,” “anticipate,” “estimate,” “plan,” “project,” “will,” “can have,” “likely,” “should,” “would,” “could” and other words and terms of similar meaning or the negative thereof. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the Company’s actual results, performance or achievements to be materially different from the expected results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which it will operate in the future. THE INFORMATION WITH RESPECT TO ANY PROJECTIONS PRESENTED HEREIN IS BASED ON A NUMBER OF ASSUMPTIONS ABOUT FUTURE EVENTS AND IS SUBJECT TO SIGNIFICANT ECONOMIC AND COMPETITIVE UNCERTAINTY AND OTHER CONTINGENCIES, NONE OF WHICH CAN BE PREDICTED WITH ANY CERTAINTY AND SOME OF WHICH ARE BEYOND THE CONTROL OF THE COMPANY. THERE CAN BE NO ASSURANCES THAT THE PROJECTIONS WILL BE REALISED, AND ACTUAL RESULTS MAY BE HIGHER OR LOWER THAN THOSE INDICATED. NONE OF THE COMPANY NOR ITS SHAREHOLDERS, DIRECTORS, OFFICERS, EMPLOYEES, ADVISORS OR AFFILIATES, OR ANY REPRESENTATIVES OR AFFILIATES OF THE FOREGOING, ASSUMES RESPONSIBILITY FOR THE ACCURACY OF THE PROJECTIONS PRESENTED HEREIN. The information contained in this communication or document, including but not limited to forward-looking statements, applies only as of the date hereof and is not intended to give any assurances as to future results. The Company expressly disclaims any obligation or undertaking to disseminate any updates or revisions to such information, including any financial data or forward-looking statements, and will not publicly release any revisions it may make to the Information that may result from any change in the Company’s expectations, any change in events, conditions or circumstances on which these forward-looking statements are based, or other events or circumstances arising after the date hereof.